It sounds like the future. But banks and Facebook have steered clear of partnerships that would integrate financial activity into the platform in such a meaningful way.

For a moment, it seemed as if Facebook could dip its toe deeper into financial services — raising questions about what such relationships would look like, and whether benefits would outweigh concerns about privacy and security.

Credit card companies, brokerages and banks have been testing artificially intelligent chatbots on Facebook Messenger, which feed customers account details and notifications about recent transactions. The Wall Street Journal has reported that Facebook had asked several major banks to provide customer information, such as account balances and credit card activity, in an attempt to offer up new services. (Financial institutions have denied handing over consumer banking data, and Facebook told CNN it was not "actively" seeking this information.)

Facebook has good reason to encourage banks to offer services on its platform: Doing so could boost the amount of time users spend on Facebook at a time when engagement is down. It could also provide access to valuable data, which would only become more vital as the company makes its own AI play.

The value proposition isn't as obvious for banks, though.

Widespread public skepticism about Facebook's protection of user data, especially in the wake of the Cambridge Analytica scandal and the site's recent hack, gives banks pause. Additionally, financial institutions have pumped money into their own apps, which users tend to view as safer.

"Facebook needs the banks more than the banks need Facebook," said Emmett Higdon, digital banking director at Javelin Strategy & Research.

The promise

Financial companies have built up some presence on Facebook in recent years.

They use the site for marketing purposes. And since customers sometimes complain about services on Facebook, banks have teams monitor the platform — though they typically direct those with problems to an official website or a secure phone line.

Some companies have gone one step further by experimenting with or deploying AI chatbots on Messenger.

PayPal users, for example, can link their accounts to Messenger, which will ping them with receipts and provide account help. American Express customers can also set up a Messenger bot to send notifications about purchases. TD Ameritrade has a chatbot that offers educational materials. Clients can also log in and make trades without leaving Messenger.

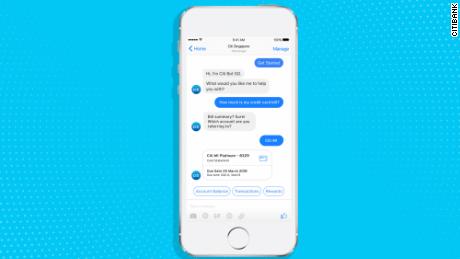

Citigroup, meanwhile, is testing a Messenger chatbot in Singapore. It lets users who verify their identities check account balances, see recent transactions and view their rewards points balance.

There is reason for the interest, even if Facebook isn't yet a strategic imperative. Because customers are already on Facebook, it makes sense to meet them there, and to encourage them to integrate money management into their everyday lives, the thinking goes.

This could help sell products down the road. And in the interim, AI could lower customer service costs.

"If a bank can offload some meaningful percentage of contact center calls onto Facebook Messenger, then there's a potential cost reduction opportunity," said Ron Shevlin, research director at Cornerstone Advisors. "And that's what Facebook [is] trying to angle for."

But researchers say it's not evident such chatbot partnerships have been game changers so far.

At least one bank, Wells Fargo, has already ended its Messenger pilot program. That project, which finished in April, had been rolled out to only 5,000 customers.

Other banks are also developing their own chatbots. Bank of America officially rolled out its AI bot, Erica, to mobile users in the spring. Capital One has a digital assistant called Eno.

"If you're Bank of America," Shevlin said, "You've got to be looking at that and saying, 'Why would I feed stuff to Facebook Messenger if it's going to disengage my customer base from Erica?'"

Privacy and security fears

Facebook's privacy and security record make the calculus look even worse, experts say.

"What's happened this year has really closed the door," said Scott Kessler, a Facebook analyst at CFRA Research. Neither Facebook nor banks would want to deal with the negative publicity, he added.

The financial services companies that have already partnered with Facebook emphasize that privacy and security are top priorities, and that what they offer via Messenger is restricted.

"Trust, security and privacy is paramount and nonnegotiable," said Sunayna Tuteja, head of strategic partnerships and emerging technologies at TD Ameritrade.

Though TD Ameritrade customers can log in and trade within the Messenger ecosystem, the company stops sharing data with Facebook at that point. It's similar to opening a private web browser with Messenger, Tuteja explained.

American Express said Facebook is only allowed to display credit card transactions to customers, and the information can't be used for any other purpose. Citi said it doesn't transmit customer names or account numbers on Messenger, which is an "opt-in" service, while PayPal said that any customer data shared with Facebook via its partnership "cannot be used for advertising or other commercial purposes." Wells Fargo said users of its shuttered pilot were cautioned not to share account numbers and other sensitive data on Facebook at the outset.

What's in it for Facebook

For Facebook, this could amount to a missed opportunity.

Though Facebook reported having more than 2.2 billion monthly users last quarter, outside analysis shows that engagement — a key metric of success — is down.

Four in 10 Facebook users over age 18 said they had taken a break from checking the platform for a period of several weeks or more in the past 12 months, according to a Pew Research Center survey released last month.

Teaming up with financial services companies could be one way to "re-engage" Facebook's user base, said Ron Shevlin, research director at Cornerstone Advisors. People regularly check account balances and transactions. It could be useful for Facebook to become part of this habit.

Above all else, financial data is an incredibly powerful tool, said Peter Wannemacher, a digital banking analyst at Forrester.

Facebook's current money-related services are limited; Messenger has enabled person-to-person payments since 2015, and merchants can accept payments from users on the platform.

"Knowing how people spend their money, or tend to spend their money, can absolutely help Facebook make its services better," Wannemacher said. Facebook could start suggesting ways for users to spend, or roll out ads that are even more personalized.

As artificial intelligence becomes more integral to its platform, such data would be a huge boon.

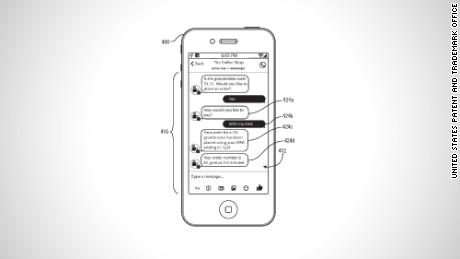

"A more expansive view of people will help those systems learn," Wannemacher said. The company has applied for a patent that details a Messenger bot that reads and responds to purchase requests from users, allowing them to order coffee and say which credit card to put it on — all within the Messenger app.

The Journal report from August said that Facebook had asked several large US banks for detailed financial data, part of Facebook's attempts to pitch banks on ways they could offer services via Messenger. A follow-up story in September said Facebook had been trying to get access to users' financial information for years.

Facebook told CNN that it was not "actively" seeking consumers' banking data, and the banks rushed to say that they'd either brushed off Facebook's requests or had been very clear with the company about the parameters of data sharing.

The "hubbub tells you a lot about the perceived risks," Wannemacher said.

The message? We're approaching this cautiously — and keeping our distance, at least for now.

Bagikan Berita Ini

0 Response to "In Facebook, banks see some opportunities — but mostly risks"

Post a Comment